Despite Inflation’s Reach, Rising Interest Rates Bring Dose of Reality to Real Estate Sector

We anticipate that interest rate hikes will lead to further performance decline in the sector, in absolute and relative terms to the broader equity markets.

/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)

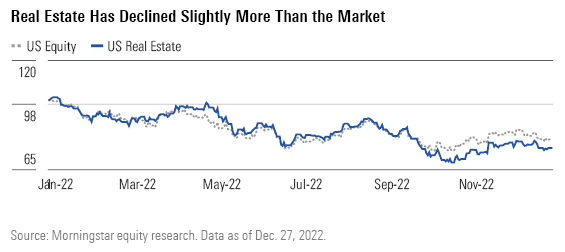

The Morningstar US Real Estate Index is down 25.31% year to date through Dec. 27, 2022, which is worse than the 19.70% decline seen by the broader U.S. equity market over the same period. The real estate sector rose 4.96% in the fourth quarter of 2022, underperforming the broader U.S. equities market that rose 6.91% quarter to date. While the real estate sector has seen negative stock performance over the past 12 months, the sector continues to report strong fundamentals growth with high inflation allowing many real estate subsectors to push rental rate increases that are well above historical averages.

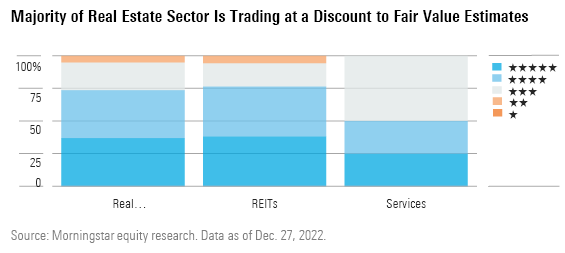

The real estate sector is currently trading significantly below our fair value estimates. The median stock valuation within real estate coverage currently trades at a 25% discount to our estimate of fair value, which is better than many other North American sectors. Currently, 71% of the real estate sector is trading in either the 5-star or 4-star range, 24% is trading in the 3-star range, and only 5% is trading in the 2-star range while no company is currently trading in the 1-star range.

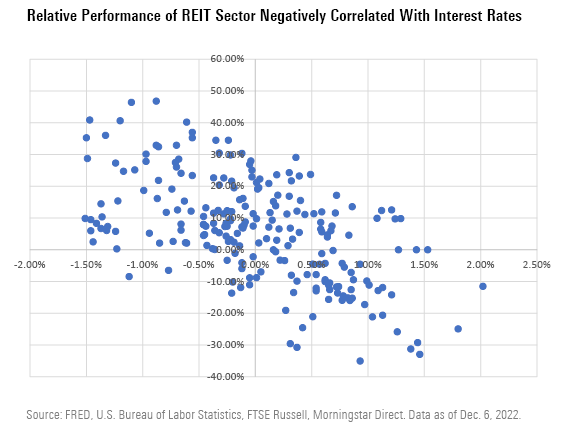

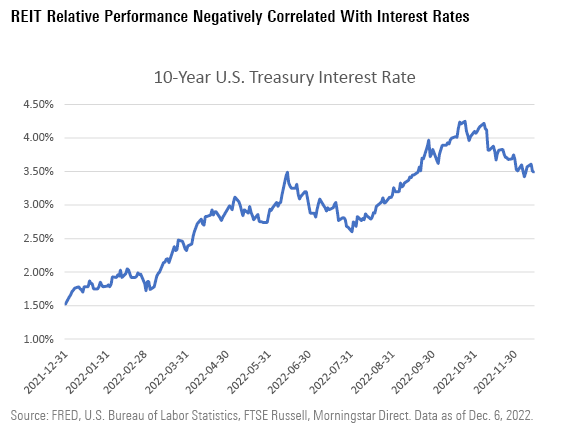

Since 2000, the relative performance of REITs compared with the broader equity market has shown a significant negative relationship to interest rate movements for the 10-year U.S. Treasury.

While many income-oriented investors favor REIT investments for their dividend payments during periods of low interest rates, rising rates cause income-oriented incomes to rotate money out of the sector and into lower-risk investments. Additionally, rising interest rates increase the debt costs many REITs rely upon to fund acquisitions and development projects, so external growth becomes less accretive to REIT cash flows as interest rates rise.

Due to the strong negative correlation, rising interest rates in 2022 have directly led to the negative performance of the real estate sector over the past 12 months. We anticipate that interest rate hikes will lead to further declines, in absolute and relative terms to the broader equity markets, for the real estate sector. However, most real estate subsectors should continue to see rate growth, and thus net operating income growth above historical average for the next quarters. Rising interest rates have limited long-term impact on REIT cashflows, so we believe many companies in the sector are trading at a discount due to short-term disruption caused by rising interest rates.

See our analysts’ Top Picks in the Real Estate Sector.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LE5DFBLC5VACTMC7JWTRIYVU5M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PJQ2TFVCOFACVODYK7FJ2Q3J2U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KPHQX3TJC5FC7OEC653JZXLIVY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)