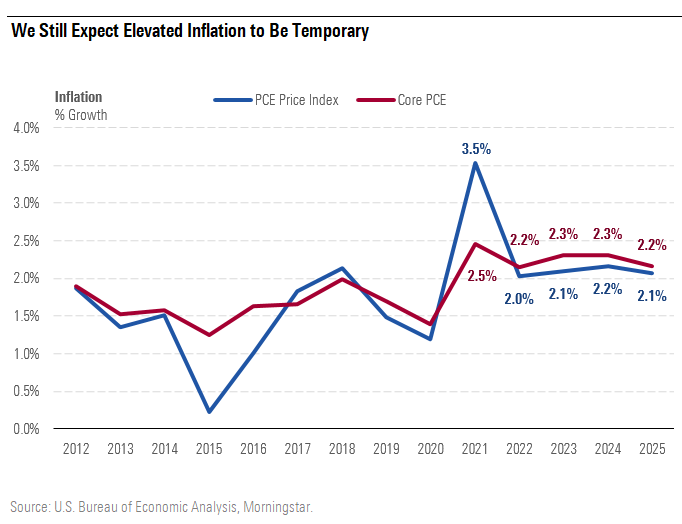

We Still Expect Elevated Inflation to Be Temporary

Once the vehicle shortage is resolved, inflation should be back on trend.

/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)

The story of inflation hasn’t changed in the last several months, in our view. The uptick in inflation has been driven primarily by the constrained supply of vehicles due to the semiconductor shortage. This shortage should be progressively resolved in the coming quarters. As such, we still expect elevated inflation to be a temporary phenomenon. We project 2.2% growth in the core Personal Consumption Expenditures Price Index over 2022-25, just modestly ahead of the Federal Reserve’s 2% target.

However, we have raised our 2021 inflation forecast to 3.5% from 2.9%, as the vehicle shortage has dragged on a little longer than we expected. This has been a product of resilient demand as much as further supply setbacks.

We Still Expect Elevated Inflation to Be Temporary

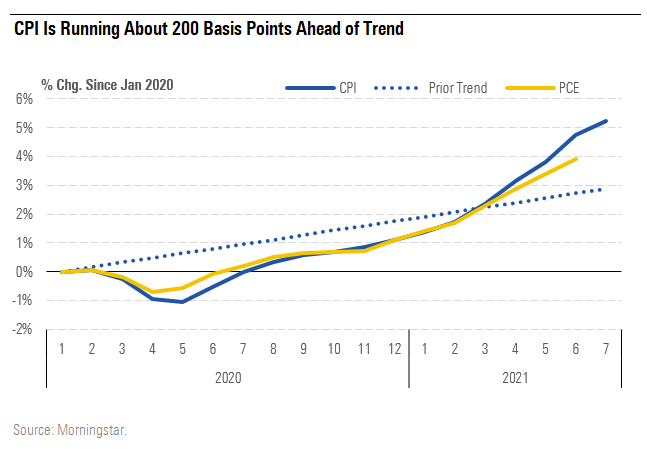

The PCE Price Index usually runs about 20-40 basis points lower than the Consumer Price Index, the inflation index commonly cited in the media. This year, we think the CPI may run about 80 basis points ahead of the PCE (posting a 4.3% inflation rate), partly driven by a higher weight on used vehicles. Our forecast focuses on the PCE for several reasons, including that it aligns methodologically with the U.S. GDP statistics.

The chart below shows the cumulative percentage change for the CPI and the PCE since January 2020. The dotted line shows the prepandemic trend for the CPI (based on the 2015-19 growth rate). While the uptick in inflation earlier in 2021 could be characterized as a return to trend, that’s clearly no longer the case. As of July 2021, the CPI is running about 200 basis points ahead of its prepandemic trend.

CPI Is Running About 200 Basis Points Ahead of Trend

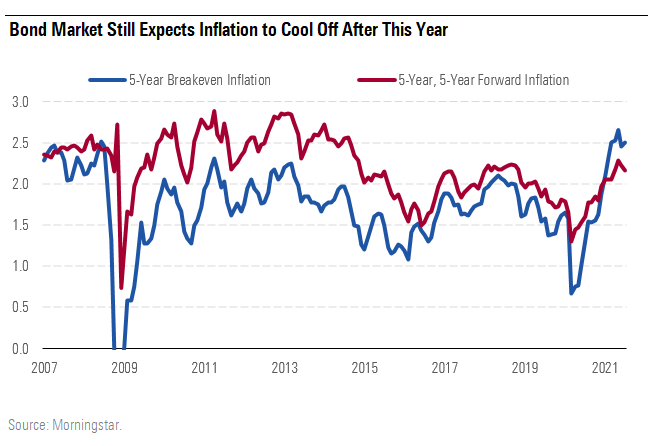

Nevertheless, the bond market seems to agree with our view that high inflation will largely be temporary. While the five-year break-even has climbed to about 2.5%--its highest since the Great Recession--it’s still only modestly above the Fed’s inflation target.

Bond Market still Expects Inflation to Cool Off After This year

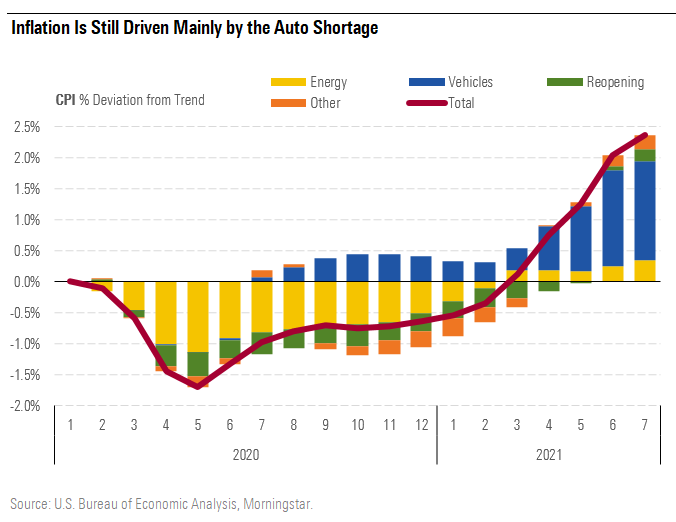

Inflation Driven Mainly by the Auto Shortage

Our confidence that high inflation will be temporary comes from the fact that it is largely contained within a single industry: autos.

Vehicles are driving the bulk of the excess inflation. The reopening industries--restaurants, hotels, air travel--have seen an increase in prices in recent months too, but that was mainly a rebound from pandemic lows. Higher oil prices are driving the energy category up, but we expect oil to eventually fall from current prices around $70 per barrel to our long-run forecast of $55 (West Texas Intermediate).

Inflation Is Still Driven Mainly by the Auto Shortage

On a month-by-month time horizon, we don’t have a strong view on exactly when the auto shortage will be resolved. The major automotive chipmakers expect to increase output sequentially in the third and fourth quarters. We see no reason the shortage won’t eventually end, even if it may not be fully resolved until 2022.

The auto story is one of exceedingly strong demand catching supply chains off guard. We’ve seen this story play out to a lesser extent in other consumer goods categories as well. As with autos, we see little reason supply won’t catch up with demand eventually. Also, pressure on supply chains should ease as consumers continue to rotate their spending from goods to services.

We Don’t Yet See Out-of-Control Wage Inflation in Most of the Economy

Sustained high inflation in the economy would have to be underpinned by commensurately high wage growth. While there do seem to be some labor supply issues in parts of the economy, we don’t see out-of-control wage inflation in most sectors.

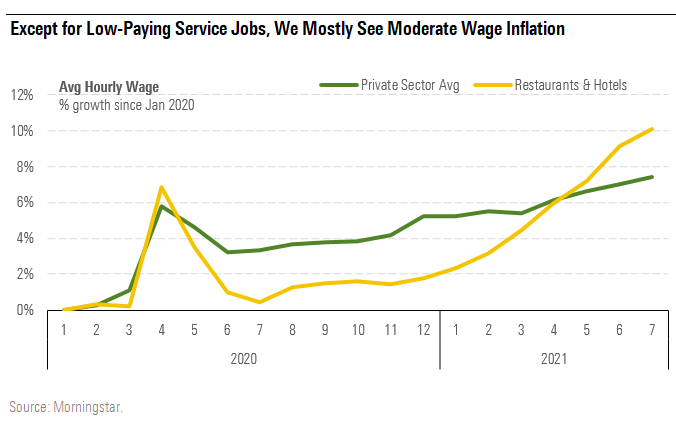

Except for Low-Paying Service Jobs, We Mostly See Moderate Wage Inflation

Wage inflation in some low-paying service jobs is on fire right now. Average hourly wages in the restaurant and hotel industries are now up about 10% versus prepandemic levels, with most of that coming in the last six months as these industries have reopened. The average worker in these industries makes about 40% below the private sector average. To the extent that boosted unemployment benefits are holding back labor supply, that impact is likely to be particularly strong in lower-wage industries like restaurants.

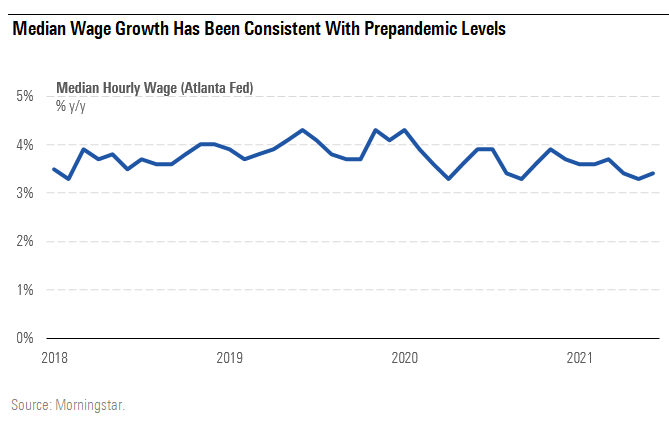

Average private sector wages don’t reflect the rate of change we’ve seen in the low-paying service jobs. Average wages are still likely distorted by the fact that lower-paid workers were disproportionately laid off during the pandemic. The Atlanta Fed’s measure of growth in median hourly wages has shown growth consistent with prepandemic rates.

Median Wage Growth Has Been Consistent With Prepandemic Levels

If boosted unemployment benefits are creating a disincentive to work, that could help account for the strong growth in employment in June and July, as around 25 states had opted out of the program by the beginning of July. Either way, the extra benefits are ending nationwide in early September.

Other reasons could also be holding labor supply back, but these are all largely temporary factors. Unavailability of childcare could be forcing working parents to stay home. Continuing fear of COVID-19 infection may be holding others back.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LE5DFBLC5VACTMC7JWTRIYVU5M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PJQ2TFVCOFACVODYK7FJ2Q3J2U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KPHQX3TJC5FC7OEC653JZXLIVY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)