5 Stocks for a Potential Debt Reckoning

These U.S. wide-moat companies may be best positioned to defend against continued inflation.

/s3.amazonaws.com/arc-authors/morningstar/35091ad9-8fe9-4231-9701-578ec44b5def.jpg)

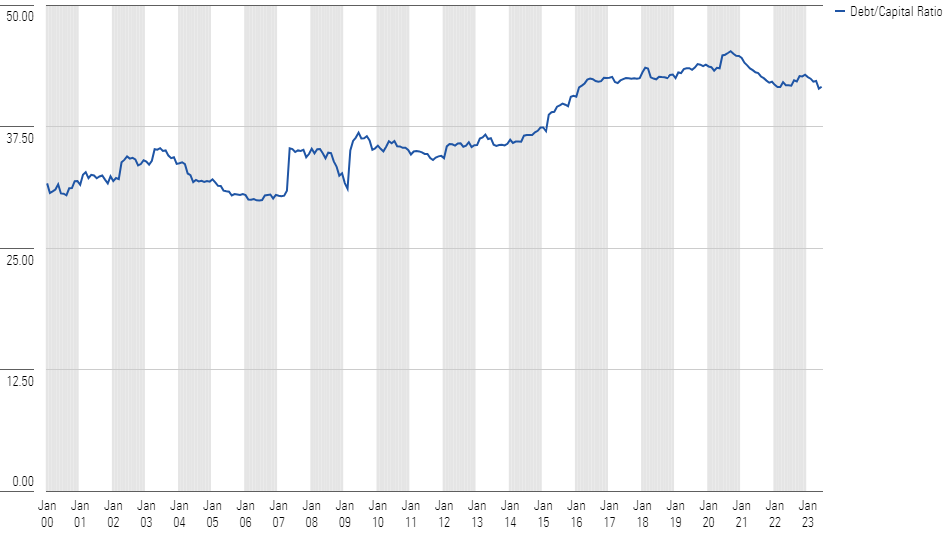

Companies have been on a debt binge over the past decade. Spurred by ultralow interest rates, the average long-term debt/capital ratio of the Morningstar US Market Index (excluding banks and other financial companies, where the ratio is not relevant) has risen to nearly 42% in June 2023 from about 36% in mid-2013 and 30% in 2000.

Average Debt/Capital Ratios Have Increased For the Morningstar US Market Index (ex Financials)

But now we’re seeing continued high inflation and uncertainty around interest rates amid broader macroeconomic concerns. While Morningstar economist Preston Caldwell is optimistic that inflation will cool and that the Federal Reserve will cut rates in response, there is a risk that ongoing job tightness will drive further price pressure, leading the Fed to keep rates higher for longer.

In this scenario, corporates could face a debt reckoning. Borrowings would need to be refinanced at a higher cost, while banks may also prove tighter with their lending capacity in a generally tough economic environment.

Given this risk, it’s worth thinking about firms that could still perform relatively well in such a period—those with pricing power through durable long-term competitive advantages, exemplary capital allocation, and minimal levels of debt (particularly debt that matures in the near term).

There are a handful of such stocks trading at reasonable margins of safety that could help investors play defense in a challenging market environment.

Be Mindful of Moats: Find Companies With Specific Sources of Competitive Advantages

The first step is to seek companies with wide Morningstar Economic Moat Ratings, or those with the most-durable long-term competitive advantages. These stocks tend to perform well in a recession and often have hallmarks such as stable demand, solid financial health, and highly profitable businesses.

In the case of dealing with higher inflation specifically, we can look a layer deeper, looking for wide-moat stocks with strong enough pricing power to pass through cost increases to consumers. Here, I’d call out three of the five moat sources as those most closely linked to pricing power: intangible assets, switching costs, or efficient scale. Each of these moat sources encourages customers to pay more, either through perceived or real product quality advantages, challenges in moving to worthy alternatives, or simply limited choice for substitutes.

Why not also look to moats driven by a network effect or cost advantage, the other two sources of competitive advantages that Morningstar equity analysts have identified? Both could be argued to be helpful in an inflation-driven recession, but I’d point out that the former is more focused on building competitive advantages through adding new clients, suppliers, or other network participants, while the latter is, not surprisingly, more focused on cost containment than raising prices.

Look for Solid Capital Allocators and Avoid Very High Uncertainty

To continue our journey, we can next look to two additional Morningstar equity research data points: the Capital Allocation Rating and the Uncertainty Rating.

Here, we can seek firms with an Exemplary Capital Allocation Rating, as we want to have confidence that companies will continue to manage their balance sheets and cash flows appropriately. After all, we don’t want to invest in another situation like Bed Bath & Beyond’s buyback woes.

In this endeavor, I recommend also avoiding stocks with a Very High Uncertainty Rating. While this is already included as part of the Morningstar Rating for stocks calculation, I think it’s worthy to concentrate even further on avoiding volatility given our goal to avoid companies facing potential financial distress.

Companies Can’t Run Into Debt Trouble If They Don’t Have Any

Once we’ve found high-quality businesses with wide economic moats, exemplary capital allocation, and relatively low levels of uncertainty, we can filter our list to include only companies with minimal debt levels, as well as the ability to cover near-term debt maturities should the credit markets become tight.

In my screen, I’ve included firms that have a debt/capital ratio on their balance sheets of less than the current 42% average across the U.S. market, excluding financial services. I’ve also ensured that each company’s cash level is greater than any debt due over the next year. While an imperfect metric, this ratio can help further insulate risk from any near-term credit-market woes.

To be clear, I’m not suggesting that other companies are necessarily facing tremendous financial risk. There are many other firms that also comfortably cover their near-term debt maturities, or screen as having relatively low levels of debt when looking at alternative metrics such as total market cap rather than the equity listed on their balance sheets (the market is forward-looking and may be wiser than the reported equity that sits on companies’ books). But for the sake of this search, I’ve opted to err on the side of conservatism.

Broken Record: Valuation Is Important

Finally, valuation remains critical—you may have seen me write that before. Buying a stock for considerably less than a fair estimate of its value can account for many risks a company may face (not to mention sins the firm may commit). For this reason, I’ve limited the search to stocks trading at 4- or 5-stars, suggesting a sizable margin of safety.

Putting it all together, there are five companies in the U.S. that are worth examining under this lens. The links below provide more information and a good starting point for further research.

Five Undervalued Stocks to Play Defense Against Further Inflation

5 Undervalued Dividend Stocks to Buy

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LE5DFBLC5VACTMC7JWTRIYVU5M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PJQ2TFVCOFACVODYK7FJ2Q3J2U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KPHQX3TJC5FC7OEC653JZXLIVY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35091ad9-8fe9-4231-9701-578ec44b5def.jpg)